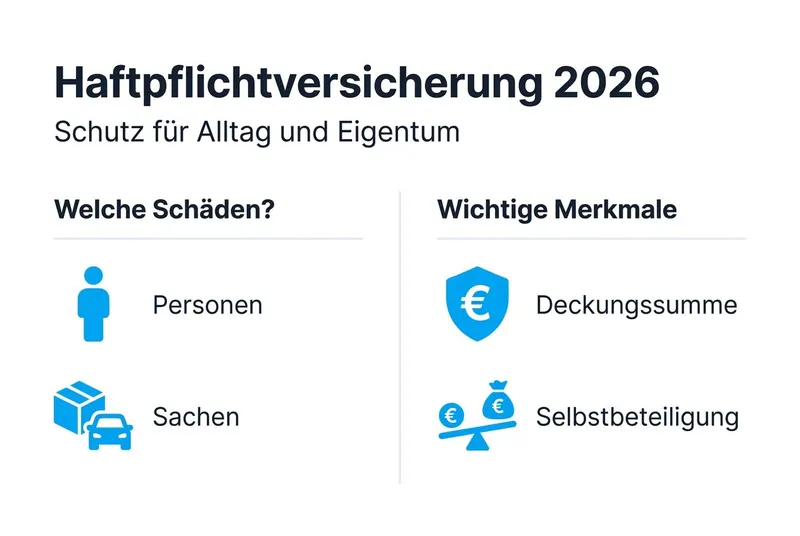

Definition and Fundamentals of Liability Insurance

Liability insurance protects you against compensation claims that third parties make against you. It covers situations where you cause damage to other people, whether through injury, damage to their property or financial disadvantages.

The insurance covers three categories of damage:

- Personal injury: Injuries or health damage to other people

- Property damage: Damage to or destruction of other people's property

- Financial losses: Financial disadvantages resulting from personal injury or property damage

The coverage amount defines the maximum amount your insurance will pay in the event of a claim. Typical coverage amounts range between 3 and 10 million euros, with higher amounts providing better protection.

Although there is no legal obligation, personal liability is one of the most important types of insurance. A single serious personal injury can result in claims amounting to millions. Without insurance, you are liable with all your assets and future income.

Pro Tip:

Look for a coverage amount of at least 10 million euros. The price difference compared to lower amounts is minimal, but the protection is significantly better. Especially with personal injuries, costs for lifelong care can quickly run into the millions.

If you need to combine different types of liability, you should also consider car liability insurance separately, as it is legally required and covers different risks.

Legal Framework and Necessity

In Germany, there is no legal obligation to have personal liability insurance, yet around 83 percent of households have taken out such a policy. This high rate shows how important consumers and experts consider this coverage.

The legal basis for compensation claims is the German Civil Code (BGB). Section 823 BGB states that anyone who negligently causes damage to another person is obligated to provide compensation. This liability is unlimited and can become existentially threatening.

| Type of Damage | Typical Costs |

|---|---|

| Water damage in rented apartment | 5,000 to 50,000 EUR |

| Bicycle accident with personal injury | 50,000 to 500,000 EUR |

| Serious personal injuries with permanent damage | 1 million EUR and more |

| Property damage to valuable items | 10,000 to 100,000 EUR |

Experts and consumer protection organizations consider personal liability to be one of the most important types of insurance. The costs of approximately 50 to 100 EUR per year are disproportionate to the financial risk without insurance.

Please note that certain professional groups additionally require professional liability insurance. Freelancers, doctors and lawyers must separately insure themselves against profession-specific risks, as personal liability does not cover these.

Differences Between Liability Types

The term "liability" encompasses various types of insurance, each covering different risk areas. This differentiation often leads to confusion among consumers.

| Liability Type | Mandatory |

|---|---|

| Personal Liability | No |

| Animal Keeper Liability | Depends on federal state |

| Property Owner Liability | No |

| Car Liability | Yes |

Personal liability covers all persons living in the household, including minor children and in some cases adult children in their first education. For dog owners, a separate animal keeper liability insurance is legally required in many federal states.

Property owners require property owner liability for rented or undeveloped properties. As an owner, you are liable for damages arising from failure to maintain traffic safety obligations.

Pro Tip:

Check exactly which liability types you actually need. Some personal liability plans include small animals such as cats or rabbits. This way you avoid double insurance and only pay for the protection you actually need.

A detailed personal liability comparison 2026 helps you find the right plan for your life situation.

Common Misconceptions and Pitfalls

Many policyholders have incorrect assumptions about what their liability insurance covers. These misconceptions can lead to unpleasant surprises in the event of a claim.

Misconception 1: Liability covers your own damage

Damage to your own property is generally excluded, as the policy only covers damage to third parties. If you damage your own smartphone or apartment furnishings, the liability insurance pays nothing.

Misconception 2: Favour damage is always covered

If you help friends move and damage their furniture, insurance coverage often does not apply. Favour damage can be covered through an additional module.

Misconception 3: Car damage is covered by personal liability

Damage caused while driving other people's vehicles is not covered by personal liability insurance. You need a separate car liability insurance for that.

Misconception 4: Intentional damage is reimbursed

Deliberately caused damage is never reimbursed. Professional risks also require a separate professional liability insurance.

Pro Tip:

Read the insurance terms and conditions thoroughly before signing a contract. Pay particular attention to exclusion clauses for favour damage and coverage for children who are not legally liable. These details make the difference between good and excellent protection.

For optimal coverage, it is worth using a affordable liability insurance comparison to find plans with comprehensive benefits. Additional information about insurance packages can be found on the topic of travel complete packages.

Find suitable providers

Compare liability insurance plans transparently and find the plan that suits you best.

Compare liability insuranceImportant Plan Features and Coverage Amounts

Choosing the right coverage amount and plan features determines the quality of your insurance protection. The principle "more expensive is better" does not automatically apply; rather, it is about matching the plan to your individual situation.

Experts recommend at least 10 million euros in coverage for secure household protection. Higher amounts of 50 or 100 million euros offer even more security at marginal additional cost.

Important additional benefits of modern liability plans:

- Loss-of-claims coverage: Steps in when someone damages you but is not insured themselves

- Key loss: Covers costs for changing lock systems if you lose a work key

- Children not legally liable: Protects against claims for damage caused by children under 7

- Voluntary activities: Covers damage during charitable engagement

- Rental property damage: Covers damage to rented apartments or holiday homes

The costs for liability insurance vary significantly depending on the scope of coverage. Basic policies are available from 40 EUR per year, while premium plans with comprehensive additional benefits cost approximately 80 to 120 EUR per year.

When evaluating cost-effectiveness, you should consider the deductible. Plans without a deductible are usually more expensive but also provide full protection for minor claims. Families benefit from plans that include all household members.

A well-founded cost-benefit analysis helps to find the optimal balance between premium and coverage.

Comparison and Plan Selection

Online comparison portals have revolutionized the search for the optimal liability insurance. Comparison portals enable significant savings on insurance through transparent comparison of hundreds of plans.

How to use comparison portals effectively:

| Comparison Criterion | What to Look For |

|---|---|

| Coverage amount | At least 10 million EUR |

| Annual premium | Check price-performance ratio |

| Deductible | 0 EUR or max. 150 EUR |

| Additional benefits | Key loss, loss-of-claims, rental property |

| Cancellation period | 3 months before year-end is typical |

| Customer reviews | At least 4 out of 5 stars |

Pro Tip:

Perform a plan comparison annually, even if you are already insured. Insurers regularly adjust their terms, and by switching you can often save significantly or receive better benefits without additional costs.

Use specialized portals for an affordable liability insurance comparison. Many platforms also offer a comprehensive overview of all insurance types, so you can optimize multiple policies simultaneously. Just as with comparing travel offers, the effort of thorough research also pays off with insurance.

Claim Settlement and Practical Tips

In the event of a claim, quick and correct action is essential. Claims should be reported within 7 days to avoid complications.

Step by step for a liability claim:

After notification, your insurer checks whether you are actually liable and whether the damage is covered by the policy. For legitimate claims, they settle directly with the injured party. For unjustified claims, they defend against them, if necessary in court.

Keep all claim-related documents at least until the settlement is complete. Proactive communication with your insurer significantly speeds up the process.

Our Recommendation for Your Liability Protection

Now that you know the fundamentals, differences and selection criteria for liability insurance, it is time for practical implementation. meinetarife24.de offers you the ideal platform for an independent and comprehensive insurance comparison.

With our personal liability comparison 2026 you will find the optimal plan in just a few minutes. Through meinetarife24 you can also optimize electricity, gas and other insurance. The comparison is free, non-binding and GDPR-compliant.

Compare now