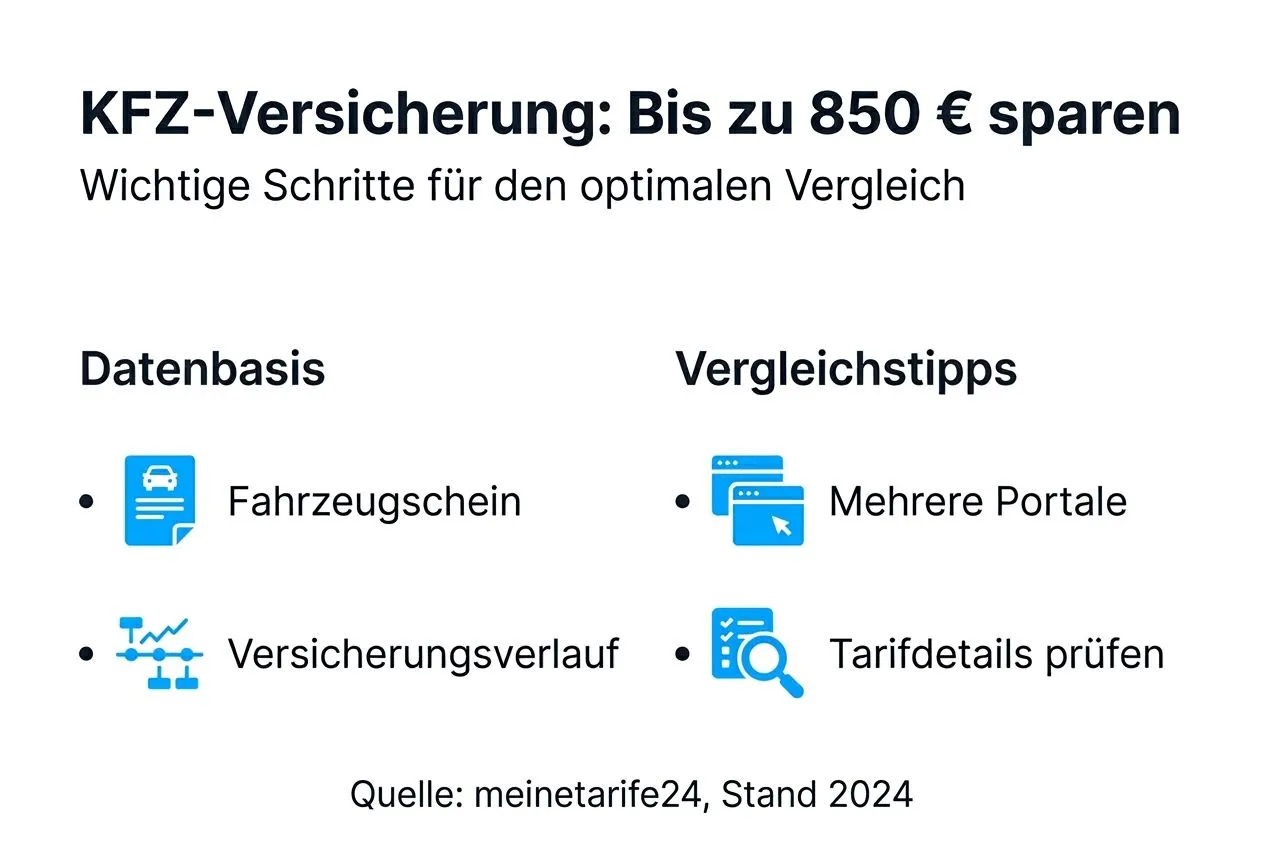

Preparation: What You Need for a Car Insurance Comparison

Before you start comparing, gather all relevant documents and information. Thorough preparation is the key to accurate results and prevents having to correct things later.

You will need the following documents and information:

- Vehicle registration certificate (Zulassungsbescheinigung Teil 1) with complete vehicle data including key number and first registration date

- Last insurance statement to determine your current no-claims class (SF-Klasse)

- Personal data such as date of birth, driving license date, and residential address for accurate premium calculation

- Realistic information on annual mileage and driver circle (just you or additional drivers)

- Cancellation deadlines of your existing contract, usually November 30 for the main due date

Entering this data accurately ensures precise premium estimates and prevents surprises later. For example, if you provide the wrong no-claims class, you will receive unrealistic offers that won't hold up at contract signing.

Pro Tip:

Photograph all relevant documents with your smartphone so you have all data at hand during the online comparison. This saves time and avoids input errors.

Use the Car Insurance Price Comparison for an initial overview of available offers.

Understanding Type and Regional Classes

Type and regional classes are among the most important factors determining your insurance premium. Without understanding these classes, you cannot properly interpret comparison results.

Type classes (Typklassen) evaluate the risk and average repair costs of your vehicle model. The classification ranges from class 10 (lowest risk) to class 34 (highest risk) and is adjusted annually by the German Insurance Association (GDV).

Regional classes depend on your registration location. Urban districts with high accident rates or theft rates lead to higher classes than rural regions. For 2026, type and regional classes were adjusted for over 10 million vehicles, resulting in significant premium changes.

| Type Class | Regional Class | Example Annual Liability Premium |

|---|---|---|

| 18 | 3 | 420 EUR |

| 18 | 8 | 580 EUR |

| 26 | 3 | 640 EUR |

| 26 | 8 | 850 EUR |

As the table shows, different combinations of type and regional classes can make a difference of several hundred euros.

Learn about the current Type Classes 2026 and regional classes before getting quotes.

Step-by-Step Comparison Method with Multiple Portals

A successful comparison follows a clear structure and uses multiple sources. This way you maximize your chances of finding the best tariff for your needs.

How to compare correctly:

Comparing on multiple portals significantly increases your chances of finding cheap tariffs, because not all insurers are present on every platform.

Pro Tip:

Run the comparison at different times of day. Some portals show dynamic prices or time-limited special offers that you might otherwise miss.

Use the Insurance Comparison effectively and also consider online comparison tips.

Evaluating Tariff Details and Additional Services

It's not just about the price - the included services determine whether a tariff is truly affordable. Understand the differences between insurance types and evaluate extras strategically.

Liability insurance (Haftpflicht) is legally required and covers damages you cause to others. Partial comprehensive (Teilkasko) extends protection to theft, glass breakage, and natural events like hail. Full comprehensive (Vollkasko) additionally covers self-inflicted accident damage and vandalism.

Important additional services overview:

Many tariffs already cover common damage cases like wildlife and marten damage in partial comprehensive insurance.

Pro Tip:

For new cars, full comprehensive insurance with a low deductible is recommended. For vehicles over ten years old, basic liability insurance is usually sufficient as the replacement value is low.

Check the benefits and additional services of different tariffs to find the right combination for you.

Compare Car Insurance Now

Find the most affordable insurance for your vehicle - independent and transparent.

Compare InsuranceCommon Mistakes When Comparing and How to Avoid Them

Many consumers make avoidable mistakes when comparing that lead to wrong offers or unnecessarily high costs. Know the most common pitfalls and avoid them strategically.

Common error sources:

- Entering wrong or outdated no-claims class: About 35 percent of all users make mistakes here, leading to unrealistic offers.

- Providing unrealistic mileage: If you drive 20,000 km but state only 10,000 km, you risk contract penalties in case of a claim.

- Defining driver circle too broadly or narrowly: A restricted driver circle saves money, but only if no additional people actually drive the car.

- Ignoring cancellation deadlines: Missing the deadline means paying too much for another full year.

- Using only one portal: Limiting yourself to one source often means missing better offers from other insurers.

Avoid these pitfalls by verifying every value before entering it and allowing enough time for the comparison.

Make sure to check cancellation deadlines to switch in time and not miss savings opportunities.

Expected Savings and Optimization Steps

How much can you realistically save, and which factors have the greatest impact? Concrete numbers and optimization tips give you clear expectations.

Through correct comparison and targeted switching, savings of up to 850 euros per year are realistic, especially if you have never switched before. Even with smaller optimizations, many consumers achieve savings of 30 to 60 percent.

| Driver Profile | Previous Premium | New Premium | Savings |

|---|---|---|---|

| 35 years, SF 12, compact car | 680 EUR | 420 EUR | 260 EUR |

| 28 years, SF 5, mid-size car | 1,150 EUR | 720 EUR | 430 EUR |

| 50 years, SF 25, SUV | 890 EUR | 580 EUR | 310 EUR |

Additional optimization steps:

- Estimate mileage realistically and reassess when driving fewer kilometers per year

- Restrict driver circle to the main driver if others rarely use the car

- Choose annual payment instead of monthly to avoid installment surcharges

- Increase deductible if you rarely report minor damages

- Regularly compare every two years as market prices and offers change

How to Switch: Cancellation Deadlines and Special Cancellation Rights

After finding the right tariff, the actual switch follows. Knowing the legal framework ensures a smooth transition.

Switch step by step:

The switch itself usually takes just a few minutes online if you have all your data prepared. The new insurer often takes care of cancelling your old provider.

Learn more about cancellation deadlines and conveniently complete your insurance switch online.

Switch safely and affordably with meinetarife24

With the car insurance price comparison at meinetarife24, you can quickly find current tariffs and compare them transparently. The simple switch including digital cancellation assistance saves time and hassle.

Compare Now