How to Compare Car Insurance in Germany — A Step-by-Step Newcomer Guide (2026)

A practical walk-through for newcomers. Coverage types, SF-Klasse, Typklasse, Regionalklasse, provider quirks, and the mistakes that cost real money.

In short: To compare car insurance in Germany correctly, gather your vehicle documents, check your no-claims class (SF-Klasse), look up your Typklasse and Regionalklasse, then run the same profile on at least two portals before pulling a direct quote from HUK24 or DEVK. Annual liability premiums typically sit between €200 and €1,500 depending on car, region and driver. Stiftung Warentest's 2026 tariff test (161 tariffs) and Verbraucherzentrale guidance both report that households switching after several loyal years often save several hundred euros.

Most newcomers in Germany overpay for car insurance because they sign with the first quote a portal shows them. That is understandable. Insurance forms are in German, the SF-Klasse system is unfamiliar, and the Zulassungsstelle wants your eVB number before you have had time to read the small print. This guide walks you through the comparison itself: what to prepare, what to check, where the cheap quotes hide, and which mistakes will cost you later.

Key takeaways

- Your no-claims class (Schadenfreiheitsklasse, SF-Klasse) carries over between German insurers. If you have a clean driving record from another country, bring official proof when you switch.

- Typklasse and Regionalklasse are updated yearly by the GDV and can shift your premium by several hundred euros without anyone consulting you.

- Two comparison portals beats one. The big direct insurers (HUK24, DEVK) often skip listings, so check them separately.

- The 30 November cancellation deadline only covers standard cancellations. A premium hike, a vehicle change, or a total loss triggers a Sonderkündigungsrecht at any time.

- Wrong data on your application means coverage gaps. The cheapest quote stops being cheap the moment it refuses to pay out.

First decide which coverage you actually need

Comparing prices is pointless if the three tariffs you put side by side cover different things. German policies stack in three layers. Only the first one is legally required; the other two are optional and only worth paying for in specific situations.

Haftpflicht

Liability (mandatory)Covers damage you cause to other people, their cars, and their property. Without it you cannot register a car in Germany. The legal minimum is high (€7.5M personal injury, €1.22M property), but most insurers default to €100M for almost no extra cost.

Teilkasko

Partial cover (optional)Adds protection against fire, theft, weather damage, animal collisions (deer, marten bites), and broken glass. Useful for cars you would not want to scrap if they got stolen overnight.

Vollkasko

Comprehensive (optional)Includes everything Teilkasko covers plus damage you cause to your own car: accidents you are at fault for, vandalism, hit-and-run damage. Standard for leased cars and new financed vehicles.

Rule of thumb: Brand-new or financed cars usually get Vollkasko. Cars between three and eight years old often work best with Teilkasko. Once a car is around ten years old, the Vollkasko premium often exceeds what you would receive in a total-loss payout, and Teilkasko or Haftpflicht-only is the rational choice. The Types of Car Insurance Germany page goes through the trade-offs case by case.

Why most newcomers overpay on their first contract

You are new here. You need plates fast. The insurer your relocation company recommended quoted you €900, you signed, and now you are reading a different blog post six months later wondering whether that was a good deal. It probably was not.

The way premiums are calculated in Germany rewards patience. The same driver, same car, same address can pay 30–60% more or less depending on how the application is filled out and which insurers are queried. A 2024 Verbraucherzentrale comparison showed the spread between the cheapest and most expensive liability quote for an identical profile can exceed €600 per year. None of that spread is luck. It is preparation.

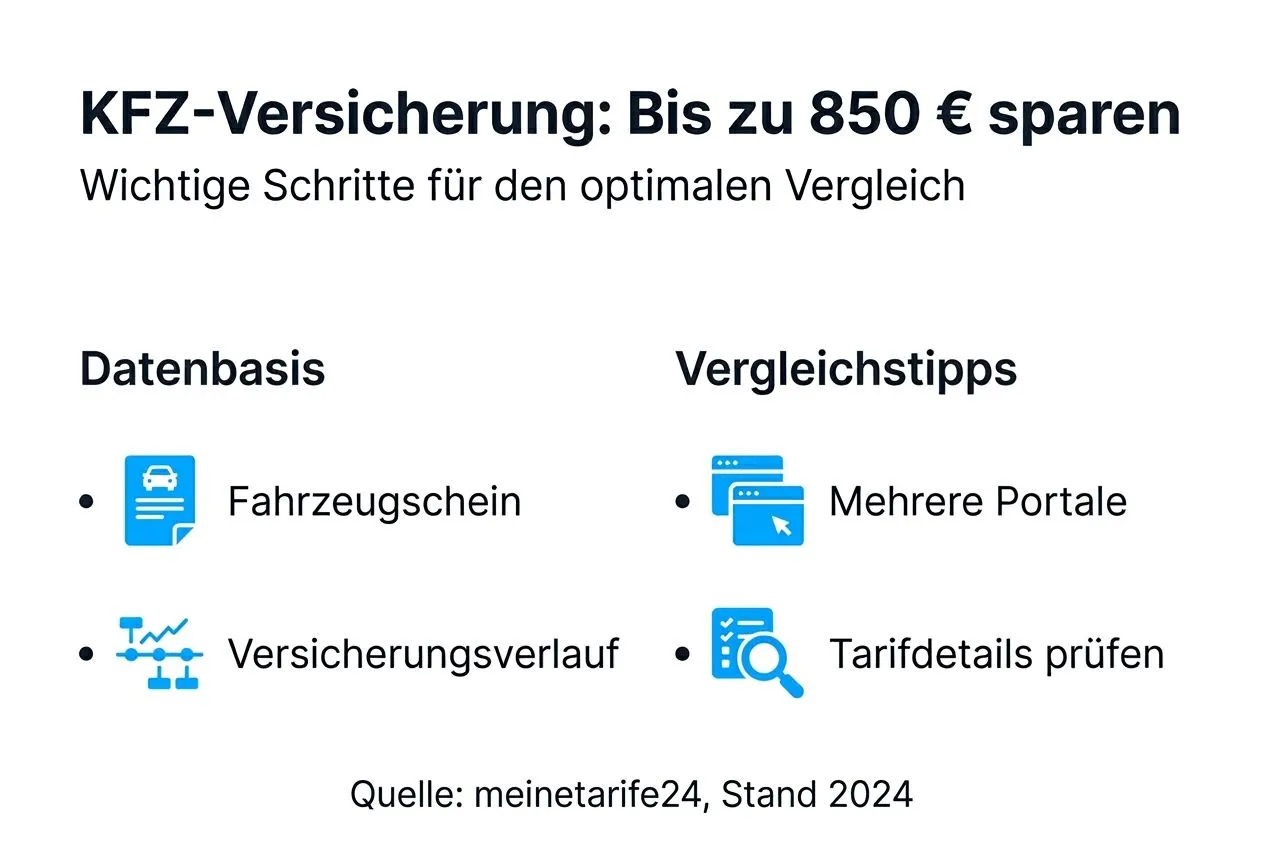

Step 1: Prepare your documents

You will move faster if you have these in one place before opening any quote tool:

- Fahrzeugschein (Zulassungsbescheinigung Teil I) — your vehicle registration certificate

- Last insurance statement (Versicherungsschein or Beitragsrechnung) — shows your current SF-Klasse

- HSN/TSN codes — Herstellerschlüsselnummer and Typschlüsselnummer, printed on the Fahrzeugschein

- Personal data: full name, date of birth, address, German driver's licence (or original licence if non-EU and not yet converted)

- Annual mileage estimate — be honest. Lying to round down by 5,000 km can void coverage in a claim.

The HSN/TSN combination determines your Typklasse. Get it wrong and every quote you see is wrong.

Step 2: Understand Typklasse and Regionalklasse

These two numbers move premiums more than anything except your SF-Klasse.

Typklasse is a 10–34 risk score the GDV assigns to your specific vehicle model each year. Cars with more claims history score higher. A Typklasse 25 small SUV can easily cost around €200/year more in liability than a Typklasse 15 hatchback of similar value. The 2026 classification covers roughly 33,000 vehicle models; the current list and explainer sits on the GDV Typklassen page.

Regionalklasse is based on the Zulassungsbezirk (registration district) of your address. A city centre with more theft and collision claims pays more than a rural district. The 2026 GDV update moved more than 10 million vehicles into a different Regionalklasse this year, often without owners noticing; premiums tend to tick up at renewal as a result. For deeper detail on how vehicle classes work, see our Type Classes 2026 guide.

| Typklasse | Regionalklasse | Example liability premium / year |

|---|---|---|

| 18 | 3 | €420 |

| 18 | 8 | €580 |

| 26 | 3 | €640 |

| 26 | 8 | €850 |

Beispielwerte / illustrative ranges based on typical 2026 market quotes. Your individual rate depends on SF-Klasse, age, mileage, deductible, and provider.

Step 3: Your SF-Klasse and foreign driving history

The Schadenfreiheitsklasse tracks how many consecutive claim-free years you have on your record. SF 0 is "new driver, no history." SF 35 is a decades-long clean record and means a discount of around 75% off the base premium for many insurers (the exact Sondertarif rules vary by provider).

If you held insurance in your name in another EU country, many German insurers will accept a Schadenfreiheitsbescheinigung from your previous insurer and translate years into a partial SF-Klasse. Non-EU records are accepted by a smaller list of insurers (HUK-Coburg, Allianz, and AXA among them in 2026; confirm at quote time). Either way, the original letter from your old insurer, translated if needed, is what unlocks the discount.

Common newcomer mistake: Many drivers do not ask their previous insurer for proof and start at SF 0 by default. This is the single most expensive misstep you can make on a German car insurance application.

Step 4: Run quotes on at least two portals (and one direct insurer)

No portal lists every insurer. CHECK24 carries a wide network. Verivox carries a different network. Tarifcheck a third. Direct-only providers like HUK24 and DEVK Direkt are sometimes excluded from one or two of these. To see the real price floor you compare on at least two portals and also pull a direct quote from a direct insurer separately.

How to do it without making the data drift:

- 1Start on a comparison portal with broad coverage to map the field.

- 2Cross-check on a second portal and note any new insurers that appear.

- 3Get a direct quote from HUK24 or DEVK on their own site.

- 4Enter the same data every time: SF-Klasse, mileage, garage usage, driver circle. Double-check each field.

- 5If the same input gives you a €200 spread between portals, something is being entered differently. Find the drift before you sign.

Provider positioning — what to expect from each channel

The German market has hundreds of carriers, but most expat-relevant quotes come from a handful of business models. The labels matter more than brand recognition: a digital direct insurer in 2026 is structurally cheaper than a broker-led product, all else equal, because the cost stack is shorter. The note about English is what trips most newcomers — the providers with the lowest sticker price usually do not staff English call centres.

| Provider / group | Channel | What that means for you |

|---|---|---|

| HUK24 HUK-Coburg group | Online-only direct insurer | Lower premiums in many quote tests because there is no broker layer. English website is limited; quote flow is German. |

| DEVK Cooperative insurer | Mixed: branches + online | Service-led positioning. Branch network is useful if you prefer paperwork in person. |

| Allianz Direct (DA Direkt) Allianz group | Online direct insurer | Web-based application; one of the few direct insurers historically offering an English flow on portal aggregators. |

| Allianz / AXA (broker channel) Multi-line insurers | Broker and direct | Wider product range and physical agents. Premiums on identical risk profiles tend to be higher than digital-only direct insurers. |

Positioning summary only. Quality of service depends on the specific tariff and the year — check the latest Stiftung Warentest Kfz-Versicherungsvergleich before deciding.

Step 5: Tariff details that matter more than you would think

The headline premium is not the contract. Read the offer terms:

- Werkstattbindung (workshop binding): Accepting that the insurer chooses the body shop can lower the premium by around 10–20% according to ADAC and Stiftung Warentest comparisons. Often a fair trade if you do not have a preferred shop.

- Selbstbeteiligung (deductible): Raising your Teilkasko deductible from €150 to €500 typically saves €30–€60/year. Raising Vollkasko from €300 to €1,000 saves more. Pick a deductible you can actually pay if your car gets stolen tomorrow.

- Fahrerkreis (driver circle): Listing "only me" is cheapest. "Me and spouse" is slightly more. "Any driver" can double the premium. Do not list more drivers than you actually use.

- Wildschadenversicherung: Teilkasko covers collisions with deer and similar. Some tariffs extend this to all wild animals. Worth checking if you drive rural roads.

- Schutzbrief (roadside assistance): Around €30/year. The ADAC Plus card overlaps with most of what this offers, so check before paying twice.

Step 6: Common mistakes when comparing

The portals make it easy to enter your data fast. Easy is not the same as correct. The mistakes that come up most:

- ×Entering the wrong SF-Klasse. Read it off your Versicherungsschein. Do not guess.

- ×Rounding mileage down. Insurers reconcile mileage at renewal and back-bill you. The "savings" reverse later.

- ×Selecting "Halter = Fahrer" when a spouse or partner also drives. This is a contract breach if the spouse is at fault.

- ×Skipping the deductible question. Default deductibles are usually not optimal.

- ×Comparing only on one portal. The cheapest provider on portal A often is not listed on portal B at all.

Step 7: Realistic savings and how to get them

For 2026 quotes, annual liability premiums for most expats land between €200 and €1,500. The wide spread is mostly driven by Typklasse and Regionalklasse, with SF-Klasse layered on top. The Verbraucherzentrale Kfz-Versicherung review guide and the annual Finanztip Kfz-Versicherung guide both report that households who have stayed on the same contract for three or more years usually find several hundred euros of savings when they finally compare. A few illustrative examples (Beispielwerte, based on typical 2026 quotes):

- 35-year-old, SF 12, compact car, urban Regionalklasse 8: €680 → €420 (€260 saved)

- 28-year-old, SF 5, mid-size sedan: €1,150 → €720 (€430 saved)

- 50-year-old, SF 25, SUV: €890 → €580 (€310 saved)

The pattern: newer drivers in expensive Regionalklassen often save the most, because their initial premiums had the most slack in them.

Step 8: How to switch — deadlines and the eVB number

Standard cancellation deadline is 30 November for a contract that ends on 31 December. Miss it and you wait another year. But §11 VVG and most insurer terms give you a Sonderkündigungsrecht if any of these happen during the contract year:

- Your insurer raises your premium without you adding coverage

- You change vehicles

- A claim is processed

- Your insurer changes its terms

The Sonderkündigungsrecht usually has a one-month window from the trigger event. Use it.

When you sign with a new insurer, ask for the eVB-Nummer (elektronische Versicherungsbestätigung). Seven digits. Your new insurer issues it by email, often within minutes. The Zulassungsstelle will not register your car without it. Plates will not issue. The eVB does not activate coverage by itself; coverage starts when the car is registered.

Verified sources

- GDV — Typklassen kurz erklärt

Official explainer from the German Insurance Association on how Typklassen are calculated each year

- ADAC — Kfz-Versicherung Vergleich

Germany's largest automobile club, independent comparison guidance

- Stiftung Warentest — Kfz-Versicherungsvergleich

Independent consumer test of 161 Kfz-Versicherung tariffs for 2026

- Verbraucherzentrale — Kfz-Versicherung überprüfen

Consumer advocacy organisation on how reviewing your tariff can save several hundred euros

- Finanztip — Kfz-Versicherung

Independent financial-advice site with practical switching guides and savings analysis

- ADAC — Sonderkündigungsrecht Kfz

Official ADAC guide on when you have a special right to cancel mid-year

Ready to compare?

When you have your Fahrzeugschein, your last Versicherungsschein, and your annual mileage in front of you, the comparison takes about ten minutes. Free, no commitment, no Schufa check needed for car insurance.

Compare car insurance quotesFrequently asked questions

Newcomer FAQ — questions specific to expats

The five questions that come up most often from newcomers and international residents.

Recommended next

- Type Classes 2026: Car Insurance Guide for Germany

- Regional Classes 2026: How Location Determines Your Car Insurance

- SF-Klasse Car Insurance Germany — No-Claims Bonus Guide

- Car Insurance Germany — Expat Guide 2026

- Instant Car Insurance Germany — eVB in 5 Minutes

- Car Insurance Premiums 2026: Costs and Savings for Expats

Available in other languages

One last thing

The right comparison is worth the ten minutes it takes. Get it done before 30 November and you start the new year with a tariff that fits your real driving, not last year's marketing.

Start the comparison