Risk Protection Definition 2026: A Guide for Expats in Germany

Living in Germany without risk protection (Risikoabsicherung) is financially fragile. A serious accident, illness or death in the family can endanger your entire existence within months. This guide explains in plain English what risk protection means in Germany, which forms exist, which strategies work, and which mistakes you should avoid, with a focus on newcomers and international families.

Updated: 26 May 2026 · meinetarife24 editorial · Sources: BaFin, GDV, Verbraucherzentrale

Key Takeaways

- Definition: Risk protection is the deliberate protection against financial consequences of unexpected events through insurance, reserves or the conscious decision to bear small risks yourself.

- Prioritisation: Existential risks (income, death cover, liability) take priority over property such as household contents or car insurance.

- Four strategies: Avoidance, reduction, transfer (via insurance) and conscious acceptance form the cornerstones of any risk steering.

- Dynamic adjustment: Cover must grow with life events such as marriage, birth or a pay rise. A five-year-old policy often has gaps today.

- Newcomer note: A German registered address and a valid residence permit unlock most term life, liability and disability policies. No Schufa credit check required.

What is risk protection? Definition and meaning

Risikoabsicherung (the German term for risk protection) can be summarised in one sentence: the deliberate, planned measure to limit or fully transfer the financial consequences of an unexpected loss to a third party. The term combines two ideas: "risk" describes the possibility that an unwanted event occurs; "protection" (Absicherung) describes the act of guarding against it.

The meaning of risk protection goes beyond pure insurance. It includes all measures a household uses to reduce the probability or financial impact of a loss: classic insurance policies, building cash reserves, and the conscious choice to carry small risks on your own balance sheet.

Related terms: management, diversification, force majeure

Risk protection and risk management are often confused but are not identical. Risk management is the overarching process of identification, assessment and steering. Risk protection is a specific measure within that process, guarding against the financial fallout.

Risk diversification describes spreading risks across different areas, mainly for investments. Diversification reduces unsystematic risk, but it does not eliminate general market risk. It complements risk protection but does not replace it.

Legal context: force majeure clauses

An often-overlooked element of risk protection is the contractual frame. Many contracts contain so-called force majeure clauses that govern what happens during unforeseeable events such as natural disasters or pandemics. German law does not have a single definition of force majeure, as each contract regulates this individually. So when you sign insurance or service contracts in Germany, read the exclusion clauses carefully.

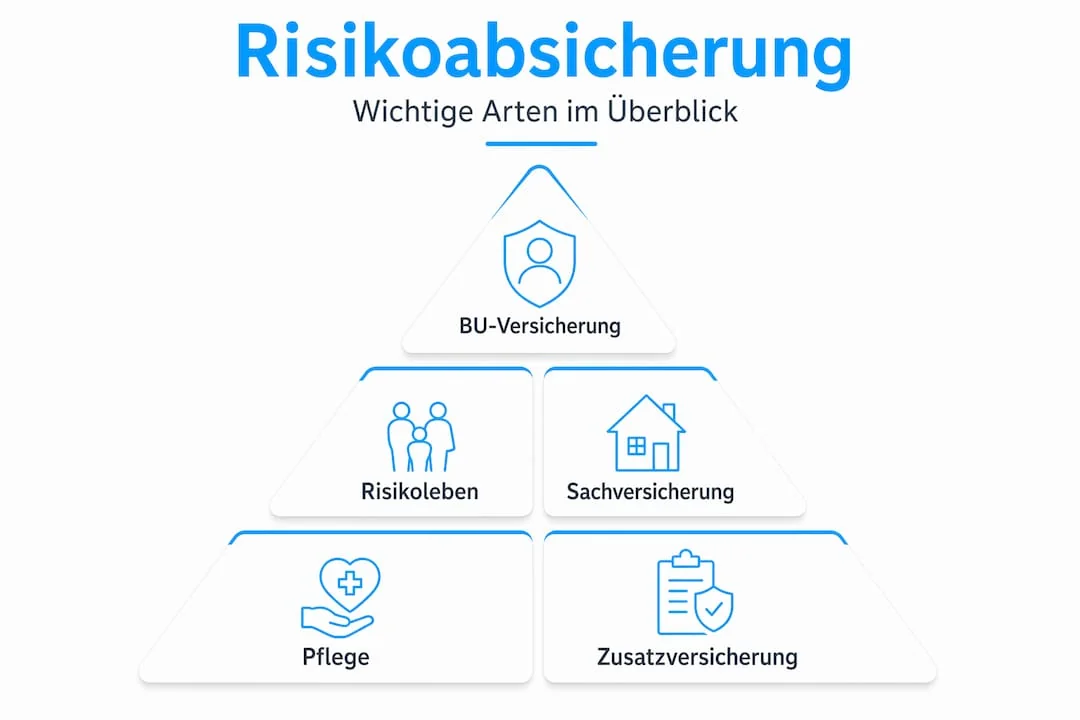

Key forms of risk protection

The forms of risk protection available to private individuals in Germany can be sorted by their function. The basic rule: existential risks take priority. Anyone insuring household contents before securing their income is setting the wrong priorities.

Disability insurance (Berufsunfähigkeitsversicherung): income protection

German disability insurance (BU) is one of the most important policies for working people. Income is the basis for all other living costs, and if it disappears, rent, food and outstanding credit instalments are immediately at risk.

The Verbraucherzentrale (German consumer advice centre) recommends insuring around 80 per cent of your net income through disability insurance; some advisers even suggest your full net income. If you earn 2,500 EUR net per month, aim for roughly 2,000 EUR in monthly BU pension. A follow-up insurance guarantee lets you raise the pension later without a new medical check.

Term life insurance (Risikolebensversicherung): family protection

Term life insurance pays an agreed sum to beneficiaries in the event of death. It is especially relevant for couples with children, sole earners and people with outstanding loans. Unlike capital life insurance, it has no savings element, which is exactly why premiums are so low for the cover provided.

Property cover: household, vehicle, building

Property insurance protects material assets. It is useful, but ranks behind existential protection in the priority list.

| Type of insurance | Purpose | Priority |

|---|---|---|

| Disability insurance (BU) | Loss of income through illness or accident | Very high |

| Term life insurance | Financial protection for family in case of death | Very high |

| Private liability insurance | Protection against third-party damage claims | High |

| Long-term care insurance | Covering care costs in old age | High |

| Building insurance | Property cover against fire, water, storm | Medium |

| Household contents insurance | Movable contents | Medium |

| Car insurance (Kfz) | Liability and comprehensive vehicle cover | Legally required |

| Supplementary health insurance | Supplements statutory health insurance | As needed |

Deductibles and conscious acceptance

A deductible means you carry part of a loss yourself. This reduces the premium notably. For example, choosing a 500 EUR deductible on car insurance significantly cuts the annual cost. The strategy is sensible if you can absorb small losses yourself and invest the saved premium into your existential cover.

Strategies and methods of risk protection

Risk-protection strategies fall into four basic methods. They originate in professional risk management but apply directly to private life.

1. Risk avoidance

The risk is excluded from the outset. Anyone without a car carries no driving risk. In most areas of life, however, this strategy is not practical.

2. Risk reduction

The probability or severity of a loss is actively reduced. Smoke detectors lower the risk of fire damage, regular health check-ups catch illnesses early.

3. Risk transfer

The financial risk is passed on to an insurer. This is the most common form of risk protection in everyday life. The insurer takes on the loss in exchange for a premium.

4. Risk acceptance

The risk is borne consciously. This deliberate cost-control strategy makes sense when the premium would be disproportionate to the possible loss.

Cost-benefit rule: Marginal protection cost should stay below the marginal loss. A policy costing 300 EUR per year that covers a maximum loss of 500 EUR is not worth it. The same premium covering 100,000 EUR is a clear win.

Pro tip: Build a personal risk matrix with probability and potential loss for each line, and assign one of the four strategies to every row.

Common mistakes in risk protection

Many households make the same mistakes with risk protection. Knowing them is the first step to avoiding them.

- Securing property before existential risks: Insuring household contents and the car before taking out disability or term life insurance sets the wrong priorities. Existential risks should always come first.

- Under-insurance through lack of adjustment: Not increasing your term life cover when your first child is born leaves you under-insured. Life changes. Cover does not adjust automatically.

- Over-insurance through double cover: Some benefits are covered more than once, for example travel cancellation through credit card and an extra standalone policy. That costs premium without extra value.

- Ignoring unclear contract definitions: Force majeure or exclusion clauses often go unread, yet they can be decisive in the event of a claim.

- Treating risk protection as a one-off: Policies unreviewed for years risk hidden coverage gaps. Risk protection is an ongoing process, not a single event.

- Over-reliance on the state: Statutory pension and health insurance provide basic protection but not full cover. Relying solely on the German state safety net is a sizeable risk.

Plan your own risk protection: step by step

Risk protection follows the same principles as professional risk management: analyse, prioritise, implement, control. For private individuals the process breaks down into clear steps.

- 1Analyse your life situation. Do you have children or dependants relying on your income? Do you have running loans? How big would the damage be if you could not work for a year?

- 2Prioritise existential risks. Cover income (BU), death (term life) and long-term care first. Then liability, then property.

- 3Review existing cover. Is the protection still up to date? Are there gaps or doubled cover? Are the insured sums still adequate?

- 4Compare offers systematically. Premiums for identical cover can vary considerably. Our insurance comparison helps you save without compromising on cover.

- 5Use independent advice. For complex questions (such as BU with pre-existing conditions), an independent insurance broker is helpful. Unlike tied agents, they have no incentive to favour specific products.

- 6Schedule a regular review. At least once a year, and immediately after major life events such as marriage, birth, job change or property purchase.

Risk protection for newcomers and expats in Germany

Newcomers to Germany often ask whether existential protection is even accessible to them. The short answer: yes, in almost all cases. The prerequisites are a German registered address (Meldeadresse) and a valid residence permit or settlement permit. A German Schufa credit check is not normally required for term life, liability or disability policies because no credit is being granted.

Mind the language barrier

Health questions are asked in German. Take your time or get a translator. Wrong answers from language misunderstandings can void the policy later.

Residence permit

If your residence permit is limited in time, the insurer may request proof. This is not a disqualifier but belongs cleanly in the application.

Beneficiaries abroad

Payouts to beneficiaries abroad work, but can take a few weeks longer. Check whether double taxation on inheritance is possible before signing.

Prioritisation

For expats the same rule applies: secure income and family first, then property. Loss of income hits young international families especially hard, since family support back home is often distant.

Compare term life insurance now

Term life (Risikolebensversicherung) is one of the most important existential protections. Our calculator returns example premiums from the Tarifcheck partner network within minutes, free of charge and without permanently storing your data.

Affiliate notice: meinetarife24.de receives a commission from the Tarifcheck partner network on contract conclusion. The comparison display itself is not influenced by this.

Optimise your protection with Meinetarife24

Households that compare their insurance regularly often pay noticeably less for the same cover. On meinetarife24.de you compare tariffs from various German providers transparently and without hours of research. Disability and term life insurance in particular reward comparison: premium differences are significant while benefit differences are often small.

- Transparent results from the Tarifcheck partner network

- Short forms, a few minutes are enough

- GDPR-compliant data processing, SSL-encrypted

Frequently asked questions about risk protection

Related topics on meinetarife24.de

- Term life insurance 2026: comparison for families

- Find affordable term life insurance

- Life insurance compared: capital vs term life

- Natural-hazard insurance (Elementarschaden) guide

- Legal protection insurance comparison

- Optimise insurance cost: concrete examples

- Insurance comparison hub: all categories at a glance