Key Takeaways at a Glance

| Key Point | Details |

|---|---|

| Follow a structured approach | A step-by-step guide simplifies the selection process and saves time |

| Know the insurance types | Haftpflicht, Teilkasko, and Vollkasko offer different levels of protection for different needs |

| Use comparison tools | Online calculators provide quick access to affordable rates and transparent price comparisons |

| Avoid common mistakes | A checklist helps you avoid typical pitfalls when signing up for insurance |

| Review regularly | Annual insurance reviews ensure lasting savings and optimal coverage |

Understanding Car Insurance Basics

Before you start comparing, it is essential to understand the different insurance types and key terminology. In Germany, car insurance comes in three levels, each providing a different scope of protection.

Haftpflichtversicherung (Third-Party Liability)

Mandatory by law. This is the minimum insurance required to drive in Germany. It covers damage you cause to other vehicles, people, or property. Without it, you are not allowed to operate your vehicle on public roads. It protects you from high compensation claims if you cause an accident.

Teilkasko (Partial Coverage)

Extends protection to your own vehicle for specific events: theft, fire, glass damage, hail, storm, and wildlife collisions. This is especially useful for vehicles that still hold significant value but are not brand new. The cost of car insurance varies considerably depending on the chosen coverage scope.

Vollkasko (Comprehensive Coverage)

Offers the most complete protection. In addition to everything Teilkasko covers, it also includes own-fault accident damage and vandalism. Recommended for new cars or high-value vehicles, as it covers your own driving mistakes too. As the vehicle ages, the benefit decreases because the replacement value drops.

Key German Terms You Should Know

Selbstbeteiligung

Deductible

The amount you pay out of pocket before insurance kicks in

Schadenfreiheitsrabatt

No-Claims Discount

Discount for accident-free years that significantly lowers your premium

Regionalklasse

Regional Class

Classification based on accident frequency in your area of residence

Typklasse

Vehicle Type Class

Rating of your vehicle model based on claim frequency and repair costs

Pro Tip

Write down any terms you do not immediately understand when reading through for the first time, and clarify them before comparing. A solid basic understanding prevents you from overlooking or misinterpreting important contract details later on.

Preparation: Setting Your Personal Requirements

Before comparing rates, you need to gather your personal data and vehicle information. Personal factors like age, occupation, and claims history strongly influence your insurance premium and are essential for accurate quotes. The more complete your details, the more precise the comparison results.

Vehicle Data You Will Need

- Make, model, and exact type designation of your car

- First registration date and current mileage

- HSN and TSN from your vehicle registration document (Fahrzeugschein)

- Information about special equipment like navigation systems or parking assistants

Your personal details are equally important for rate calculation. Insurers consider your date of birth, as younger drivers statistically cause more accidents. Your place of residence determines the regional class (Regionalklasse), which varies depending on accident frequency in your area. Annual mileage also plays a role, since higher mileage means higher accident risk.

Special circumstances can significantly lower your premium. Do you have a garage or fixed parking spot? Is this a second vehicle? Does your car have modern safety systems like automatic emergency braking or lane departure warning? All these factors have a positive impact on your insurance contribution.

Deductible Tip

Think ahead about what deductible you can afford in case of a claim. A higher deductible noticeably lowers your monthly premium but means higher out-of-pocket costs in case of damage. For most drivers, 150 to 300 Euro for Teilkasko and 300 to 500 Euro for Vollkasko is a good balance.

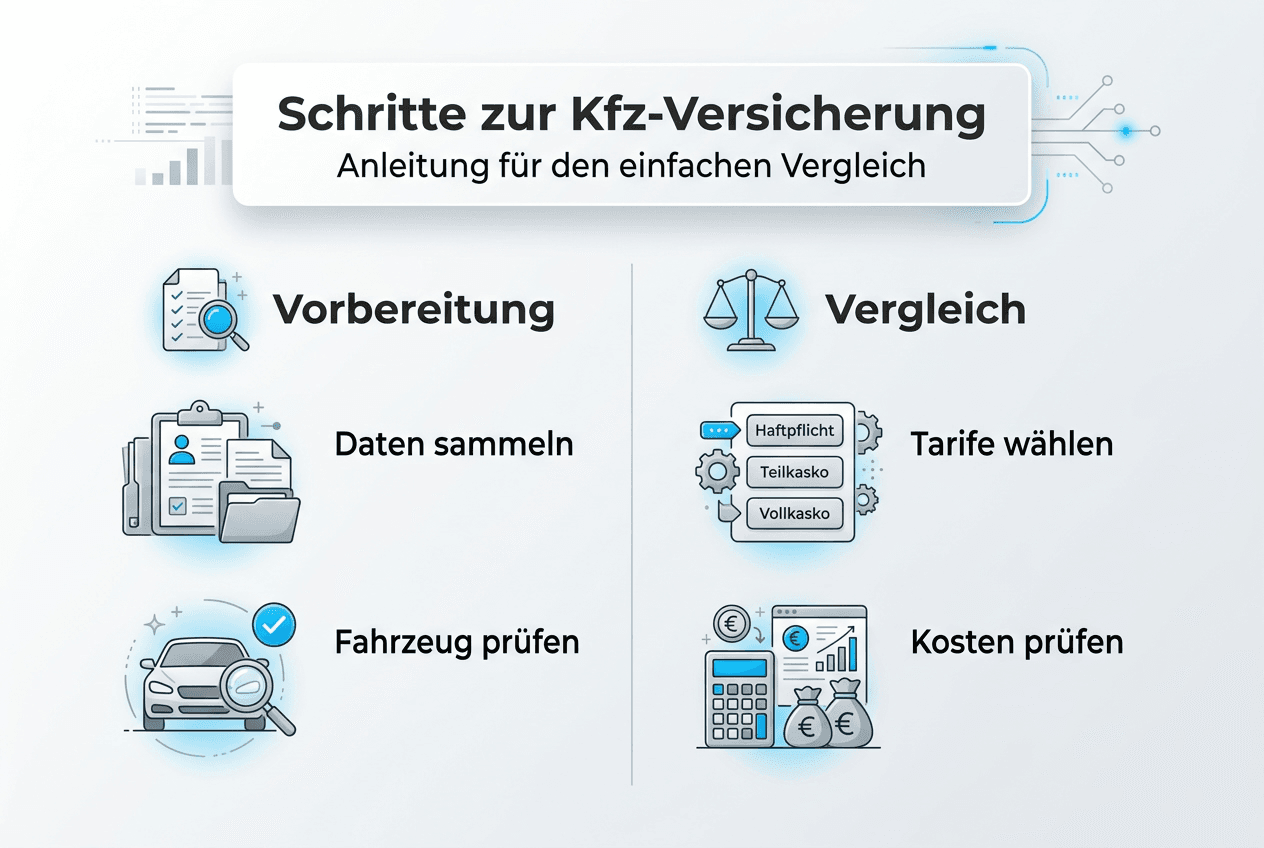

Selection and Comparison: Comparing Step by Step

Now the actual comparison process begins, where you identify and evaluate suitable rates. Online comparison portals help you quickly find affordable and fitting car insurance policies. Approach this systematically to avoid missing important details.

Enter Your Rate Criteria

Open a comparison calculator and enter all your prepared data completely. Pay special attention to correct details for your no-claims class (Schadenfreiheitsklasse), as this has the greatest impact on your premium. Select your desired coverage level.

Review the Offers

Do not sort results only by the cheapest price. Also consider the scope of coverage and customer reviews. A low premium is useless if important benefits are missing when you need them or if claims processing is slow.

Compare Insurance Coverage

Check exactly which benefits are included in each policy. Some insurers offer extras like no-claims protection (Rabattschutz), extended wildlife damage coverage, or waiver of gross negligence objection. These can be valuable in an emergency.

Identify Discounts

Many insurers offer special rates for certain professions, garage users, or when bundling multiple contracts. Check which discounts apply to your situation when comparing policies.

Make Your Final Decision

Choose the policy with the best value for your individual situation. The cheapest option is not always the best if important coverage is missing.

Pro Tip

Create a comparison table with the three to five most interesting offers and note specific coverage features alongside the price. This helps you keep track and make a well-informed decision.

| Criterion | Policy A | Policy B | Policy C |

|---|---|---|---|

| Annual Premium | 420 Euro | 385 Euro | 450 Euro |

| Deductible | 300 Euro | 500 Euro | 150 Euro |

| No-Claims Protection | Yes | No | Yes |

| Workshop Restriction | No | Yes | No |

| Customer Rating | 4.2 Stars | 3.8 Stars | 4.5 Stars |

Compare Car Insurance Now

Use our free comparison tool to find the best rate for your situation. Enter your details and see transparent results in minutes.

Datenquelle & Transparenz

Die Tarifdaten auf dieser Seite werden in Echtzeit von Tarifcheck bereitgestellt. Wir greifen nicht in die Preise, Rankings oder Darstellung der Ergebnisse ein.

Unsere Rolle:

Wir bieten redaktionelle Erklärungen und Entscheidungshilfen. Die eigentliche Tarifberechnung und Vermittlung erfolgt durch unsere Partner.

Was wir nicht abdecken:

Nicht alle Anbieter am Markt sind in diesem Vergleich enthalten. Regionale Anbieter oder spezialisierte Tarife können fehlen.

Online Application and Contract Review

After deciding on a policy, the sign-up process follows, where careful attention is crucial. Many insured people make mistakes during the online application that can lead to disadvantages later. Read the contract terms thoroughly before signing.

Pay Attention to These Contract Details

Exclusions (Ausschluesse)

Which damages are explicitly not covered? Some policies exclude marten bite damage or certain natural events.

Contract Duration (Vertragslaufzeit)

Most policies run for one year with automatic renewal. Check the cancellation deadline, usually one month before contract end.

Payment Method (Zahlungsweise)

Annual payment is usually cheaper than monthly installments. Some insurers charge surcharges for installment payments.

Workshop Restriction (Werkstattbindung)

Some cheaper policies require you to use a partner workshop for repairs. This can mean limitations on your choice of garage.

Enter all personal data correctly and completely. Incorrect information can lead to loss of insurance coverage in case of a claim. Particularly critical are details about your no-claims class, driver circle, and annual mileage. If you are unsure, choose a slightly higher mileage rather than one that is too low.

eVB Number (elektronische Versicherungsbestaetigung)

After signing up, you receive the electronic insurance confirmation, the eVB number. This 7-character code is required to register your vehicle at the registration office (Zulassungsstelle). Keep all documents safe.

"A thorough review of contract terms before signing prevents unpleasant surprises in case of a claim and secures the agreed protection."

Check the confirmation email and insurance policy carefully for accuracy. Do all details match your information? Does the premium match the displayed offer? If there are discrepancies, contact the insurer immediately.

Common Mistakes and Optimization

After signing up, the work is not done. Regular insurance comparison saves money and avoids over-insurance. Review your contract at least once a year, ideally before the key date of November 30 -- the last day for regular cancellations effective at year-end.

Typical Mistakes to Avoid

Incorrect Mileage (Kilometerangaben)

Stating too low a mileage can cause problems in case of a claim.

Concealed Prior Damage (Vorschaeden)

Unreported accidents jeopardize your insurance coverage.

Missed Cancellation Deadlines (Kuendigungsfristen)

The one-month deadline before contract end must be strictly observed.

Ignoring Automatic Renewal

Without cancellation, the contract automatically continues for another year.

How to Switch to a Cheaper Provider

- 1Compare current rates no later than October or November

- 2Cancel your old contract in writing, ideally by registered mail (Einschreiben)

- 3Only sign the new contract after receiving cancellation confirmation

- 4Ensure seamless insurance coverage during the switch

- 5Inform the registration office (Zulassungsstelle) about the insurance change

Optimize your insurance to match your current life situation. Is your car driving fewer kilometers than originally stated? Have you moved? Do you now use a garage? All these changes can lower your premium. Report such changes to your insurer promptly.

When to Downgrade Coverage

For older vehicles, check whether Vollkasko is still worthwhile. As a rule of thumb: if the replacement value is below 4,000 Euro, Teilkasko is usually sufficient. For very old cars with low value, pure liability insurance may be enough. Through proactive management and regular reviews, you secure the best conditions long-term.

Save with meinetarife24 -- Your Partner for Car Insurance

You have now learned how to systematically find the right car insurance. But where do you find the best current offers for 2026? meinetarife24 provides you with exactly the tools you need for a successful comparison.

With our insurance comparison, you can conveniently compare hundreds of rates and find the best offer for your situation within minutes. The platform works with renowned partners like CHECK24 and Tarifcheck to give you access to all relevant insurers. The online process is straightforward: enter your details, compare offers, and sign up directly.

Especially practical is the car insurance comparison feature, which delivers transparent price comparisons and reveals savings potential of several hundred Euro. All tools are GDPR-compliant (DSGVO-konform) and protect your personal data. Use meinetarife24.de to optimize your car insurance today and save money long-term.

Frequently Asked Questions

What car insurance do I need at minimum in Germany?

At minimum, third-party liability insurance (Haftpflichtversicherung) is legally required, and without it you may not operate your vehicle on public roads. It covers damage you cause to other vehicles, people, or property with your car. The coverage limits are set by law and protect you against high compensation claims. For extra protection, you can add Teilkasko (partial) or Vollkasko (comprehensive) coverage.

How can I save money on car insurance?

Compare multiple providers before signing to find the best value. Use no-claims discounts (Schadenfreiheitsrabatt), which significantly reduce your premium for accident-free years. Adjust the deductible (Selbstbeteiligung) to your financial situation, as a higher deductible reduces the monthly premium noticeably. Report changes like garage use or lower mileage promptly, as these can lower costs. Pay annually instead of monthly to avoid installment surcharges.

When should I switch my car insurance?

Consider switching during annual contract reviews when you find significantly better offers with comparable or improved coverage. After major changes in your driving behavior, vehicle, or life situation, check if a different policy fits better. If your no-claims class (Schadenfreiheitsklasse) has improved or you have moved, new providers may offer more attractive rates. Always respect the cancellation deadline of one month before contract end (usually November 30 for year-end switch).

What data do I need for the online application?

You need complete vehicle details: make, model, year, HSN (manufacturer code), TSN (type code), and annual mileage. Your personal information includes name, address, date of birth, and details about the driver circle (Fahrerkreis). You must also provide your current no-claims class and desired coverage level with deductible amount. Have your payment information ready to complete the process smoothly.

Recommended Articles

Car Insurance 2026: New Laws for Consumers

Legal changes and consumer rights updates

Car Insurance 2026: Premiums and Saving Strategies

How premiums are changing and how to save

6 Car Insurance Benefits: Save More in 2026

Practical tips for maximizing savings

Compare Car Insurance

Free comparison tool for the best rates