TL;DR – the key facts in 30 seconds

TL;DR – the key facts in 30 seconds

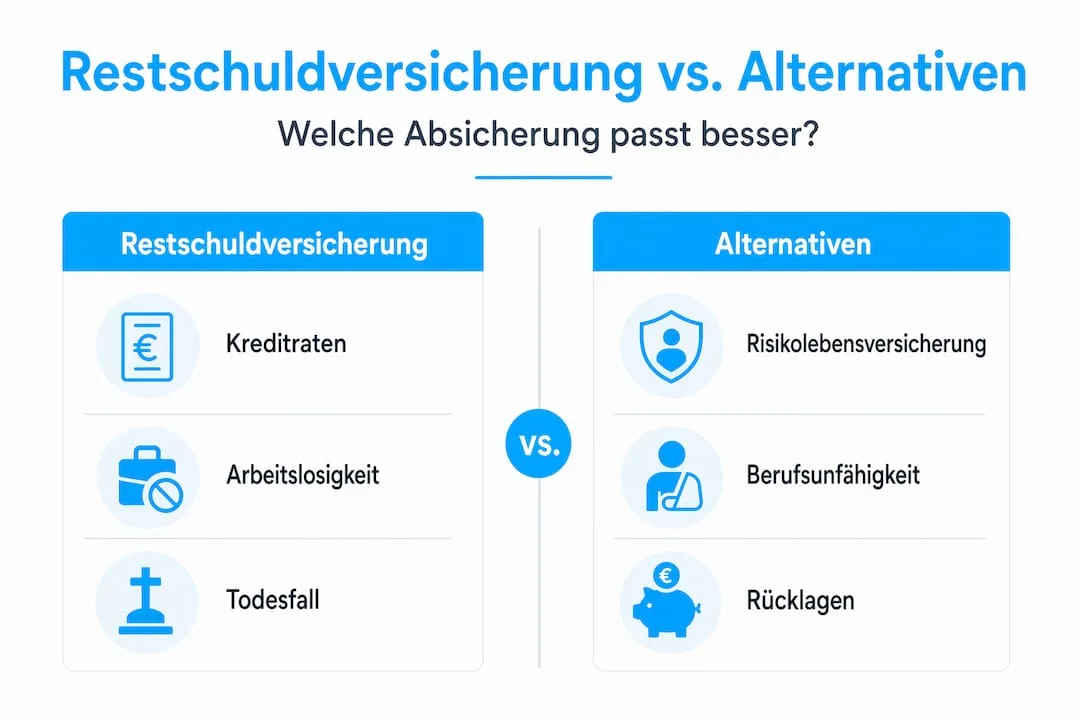

Residual debt insurance (Restschuldversicherung) is sold alongside loans in Germany but is not mandatory. It is meant to pay your instalments or wipe the remaining debt if you die, become unemployed or unable to work.

Consumer protection groups criticise high costs, opaque exclusions and frequent denials. For most expats, term life insurance + disability insurance is the better combination.

Table of contents

Most people who take out a loan in Germany run into the same scene: the bank advisor mentions a Restschuldversicherung, and suddenly it sounds essential. But what is residual debt insurance, really – and is it worth it? It is not a legally required product, yet it is routinely sold with instalment loans, mortgages and car finance. This guide explains how it works, where it fails, and what the realistic alternatives are.

Key facts at a glance

| Point | Details |

|---|---|

| Definition | Pays instalments or settles the remaining loan balance on death, unemployment or inability to work. |

| Not mandatory | No statutory obligation – evaluate it as a separate product. |

| Costs vary widely | Premiums depend on insurer, loan term and selected coverage package. |

| 7-day waiting period | Since January 2025 it can be signed only 7+ days after the loan contract. |

| Consider alternatives | Term life and disability insurance often cover more for less money. |

What residual debt insurance is

Restschuldversicherung – sometimes called Restkreditversicherung – is a form of credit protection insurance. It steps in when a borrower can no longer pay instalments because of a defined risk event. It is meant to protect both the borrower and the heirs from the financial fallout of an unexpected event. Germany's financial regulator BaFin lists it as a standalone, advice-heavy product, a hint at how carefully you should read the terms.

Which risks are covered?

- Death: the insurer settles the remaining loan balance in full and releases the heirs from the obligation.

- Involuntary unemployment: monthly instalments are taken over for a limited period after job loss.

- Inability to work: illness or accident triggers temporary takeover of the monthly payments.

The difference matters: death triggers a one-off full settlement, while unemployment or inability to work generates only temporary monthly cover. Many borrowers only discover this gap when they actually file a claim.

Where it is typically sold

- Instalment loans and consumer credit (furniture, electronics, holidays)

- Mortgages and home financing

- Car loans and vehicle financing

The legal framework since January 2025

A detail few borrowers know: since January 2025, residual debt insurance on a consumer loan can be signed only one week (7 days) after the loan contract itself. The rule lives in § 7a of the Insurance Contract Act (VVG) and stops banks from selling the policy under time pressure during the loan meeting. If the waiting period is ignored, the insurance contract is void.

One important exception: this waiting period and the ban on tying the loan to the insurance apply to ordinary consumer loans (instalment and consumer credit). With a mortgage (Immobiliar-Verbraucherdarlehen), the bank may still require residual debt insurance, and the 7-day rule does not apply.

Pro tip for expats

Pro tip for expats

Cost, benefits and contract details

Premiums depend on loan amount, loan term and the protection package. A death-only package is cheaper than a package that also covers unemployment and inability to work.

Typical benefit examples

| Benefit | Typical amount | Duration |

|---|---|---|

| Instalment cover during unemployment | up to ~€1,500/month | limited, contract-dependent |

| Instalment cover during inability to work | up to ~€1,500/month | limited, contract-dependent |

| Death benefit (loan settlement) | up to ~€120,000 remaining debt | one-off, full settlement |

| Maximum contract term | loans up to 120 months | tied to the loan |

Indicative figures for typical instalment-loan protection packages; concrete values vary by insurer.

These are indicative figures – they vary substantially between insurers. A side-by-side insurance comparison before signing is essential.

Exclusions and waiting periods

A common but underestimated risk: contracts include long exclusion lists and waiting periods that block payouts when it matters most. The expats most often affected are those with pre-existing conditions or fixed-term work contracts.

- Pre-existing conditions known before signing

- Self-inflicted unemployment or employee-initiated resignation

- Waiting periods of 3 to 6 months after signing

- Fixed-term employment contracts often excluded

Withdrawal right and contract design

After signing, a statutory 14-day withdrawal right applies. You can revoke without reason. Read the product information sheet carefully before you sign, especially the exclusions.

Criticism, risks and alternatives

Residual debt insurance has a poor reputation in Germany – and for good reason. Consumer advocates have warned for years that the product is often expensive, opaque and disappointing at claim time.

"Residual debt insurance is often expensive and pays out little." That is roughly how the Verbraucherzentrale (Germany's consumer advice centre) sums it up, recommending term life and disability cover instead.

The most common criticisms

- High cost vs. benefit: premiums can be a significant share of the total loan cost.

- Opaque clauses: exclusions are easy to overlook and only surface at claim time.

- Sales pressure: contracts are often signed quickly during the loan meeting.

- Claim denials: rejections based on pre-existing conditions or contract exclusions are a known pattern.

The realistic alternatives

Term life insurance (Risikolebensversicherung): pays a fixed sum on death, independent of any loan. Usually cheaper and far more flexible than residual debt insurance. A current term life insurance comparison on meinetarife24 covers numerous providers.

Disability insurance (Berufsunfähigkeitsversicherung): pays a monthly pension when you can no longer work. Far broader than residual debt insurance and independent of any specific loan.

Personal savings: if you have a buffer, you can cover instalments yourself. Mortgage specialists often recommend keeping financial reserves and making special repayments over buying an expensive insurance product.

The combination: term life + disability insurance covers most relevant risks – usually for less than a Restschuldversicherung that pays out reluctantly.

Compare term life insurance now

Rather than signing the bank's residual debt insurance directly, look at a term life insurance. It is cheaper, more flexible and not bound to a single loan. Compare offers below – free, anonymous and without obligation.

Anonymous, no commitment, results within minutes.

Loading comparison...

When does residual debt insurance actually make sense?

It depends on your situation, loan size, health status and existing coverage. There are cases where it can genuinely help:

- Single income earner with family and a large loan – when no other coverage exists.

- No term life insurance yet – as a short bridge while you set one up.

- Pre-existing conditions – sometimes a simpler health check than a full term life policy.

- Short loan term – a basic protection package can be acceptable if the premium is modest.

Quick self-check

- Do you already have term life or disability insurance?

- Do you have savings to cover several monthly instalments?

- Is your job stable and permanent?

- Do you have any condition that would push up the price of an alternative policy?

- How large is the loan and how long is the term?

If you answer the first three with "yes", you very likely do not need residual debt insurance.

Practical advice

Practical advice

Editor's take

What bothers us is not the product itself – it is how it is sold. In rare cases residual debt insurance does help. Far more often, people pay premiums for years for coverage that fails the moment they need it: a pre-existing condition that was not flagged, a resignation that the insurer classifies as voluntary, a waiting period that blocks the claim.

Anyone willing to spend a few hours analysing their actual risks finds a better solution almost every time. The combination of a term life policy, a disability policy and a small cash buffer beats the all-in-one product in most life situations.

FAQ – residual debt insurance in Germany

meinetarife24 Editorial Team

Independent EditorialOur independent editorial team carefully reviews all information and regularly updates the content.

Related comparisons on meinetarife24

- Insurance comparison overview

- Term life insurance comparison

- Loan and credit comparison

- Finance products comparison

Disclaimer: This guide is general information and does not replace individual insurance or legal advice. Terms vary by insurer and personal situation. Updated 2026-06-06.