Building Insurance 2026: What It Covers and How to Save

Learn what building insurance (Wohngebäudeversicherung) in Germany really covers in 2026 and how you can save hundreds of euros annually through targeted rate comparison.

Many homeowners believe that building insurance is expensive and unnecessary. The opposite is true. This insurance protects your most valuable asset against existential damage from fire, storm, or water damage. Without it, you risk financial ruin from a single incident. In this article, you'll learn which risks building insurance covers, what rate options exist, and how you can save several hundred euros annually through targeted comparison. We clear up misconceptions and show you what really matters when taking out a policy.

Key Points About Building Insurance

Definition & Coverage

Building insurance (Wohngebäudeversicherung) protects the building itself against fire, water pipes, storm, and hail damage.

Insurance Types & Add-ons

Basic coverage handles standard risks; natural hazard coverage (Elementarschutz) extends to flooding and earthquakes.

Cost Optimization via Comparison

Rate comparisons can reduce premiums by up to 40 percent with the same coverage.

Key Contract Aspects

Underinsurance waiver and replacement value coverage are crucial contract components.

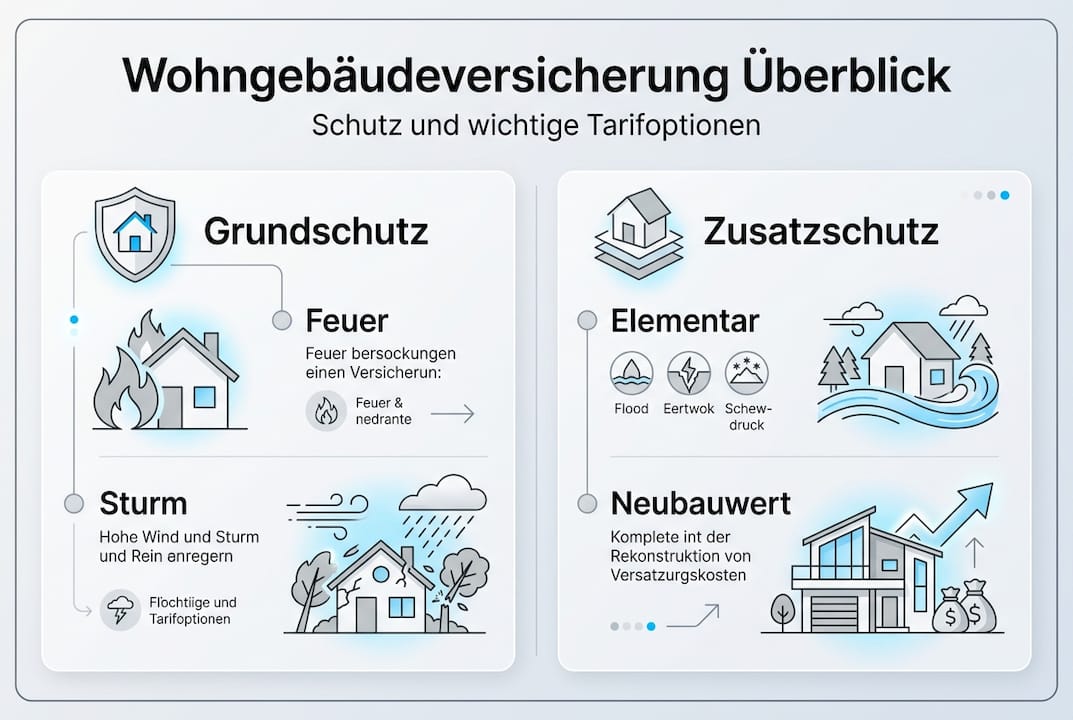

What Is Building Insurance and What Does It Cover?

Building insurance (Wohngebäudeversicherung) protects the building itself against various hazards — not the contents. It covers damage to masonry, roof, windows, and permanently installed elements like heating systems or plumbing. Building insurance covers damage from fire, storm, hail, and water pipes, which are among the most common and expensive types of damage.

For homeowners, this insurance is essential. A fire can completely destroy a single-family house, causing repair costs of several hundred thousand euros. Without insurance, you would have to pay this sum out of your own pocket. The insurance covers restoration costs, cleanup work, and even hotel costs during renovation.

It's important to distinguish it from other types of insurance. Contents insurance (Hausratversicherung) protects your possessions inside the building — furniture, electronics, and personal items. Private liability insurance covers damage you cause to others. Only building insurance protects the building structure itself.

Basic coverage includes these main risks:

Fire Damage

from fire, lightning, or explosion

Water Pipe Damage

from burst pipes or defective lines

Storm Damage

from wind force 8 on roof and facade

Hail Damage

to roof tiles, windows, and exterior walls

Additional options extend coverage. Natural hazard coverage (Elementarschutz) covers natural dangers such as flooding, heavy rain, landslides, or snow pressure. This extension is especially worthwhile in risk areas. Some insurers also offer protection against vandalism or gross negligence. Check carefully which risks are relevant in your region before booking additional modules.

Building insurance costs vary depending on building value, construction type, and location. Comparing different providers always pays off.

Important Rate Options and Coverage Scope

Rate options determine how comprehensively your building is protected and how much you receive in the event of a claim. Choosing the right options affects both your premium and your financial security. Rate options differ, for example, through natural hazard coverage or underinsurance waiver, which significantly impacts insurance protection.

Natural hazard coverage (Elementarschutz) extends basic coverage to include natural dangers. Without this option, you bear the costs of flooding or heavy rain yourself. In recent years, such events have increased dramatically. Many insurers only offer natural hazard coverage in certain risk classes — some regions are considered uninsurable.

The underinsurance waiver (Unterversicherungsverzicht) guarantees that the insurer covers the full costs in the event of a claim, even if the insured sum was set too low. Without this clause, you risk a proportional reduction in benefits. If your house is worth €400,000 but you only insured €300,000, the insurance pays only 75 percent of the damage.

Replacement value insurance (Neubauwertversicherung) replaces damaged building parts at the current new construction price, not the depreciated value. This is crucial because materials and labor costs constantly rise. In the event of total loss, you receive enough money to rebuild your house to an equivalent standard.

| Rate Option | Benefit | Typical Surcharge |

|---|---|---|

| Natural Hazard Coverage | Protection against flooding, heavy rain, landslides | 20 to 50 percent |

| Underinsurance Waiver | Full cost coverage without reduction | Included in basic rate |

| Replacement Value Coverage | Rebuild at current prices | Standard in good rates |

| Gross Negligence | Protection even when at fault | 5 to 15 percent |

Pro Tip

Skip unnecessary add-ons like glass breakage insurance if it's already included in your contents insurance. Check existing contracts carefully to avoid double insurance. Focus on essential risks like natural hazard damage and adequate insured sums.

When comparing building insurance, don't focus only on price. The contract terms are what matter. A cheap rate without an underinsurance waiver can become more expensive in the event of a claim than a slightly pricier contract with better conditions.

Also pay attention to deductibles. Some rates offer lower premiums with higher deductibles. This only pays off if you can afford several hundred or thousand euros out of pocket in the event of a claim. For most homeowners, rates without a deductible are the better choice.

How to Save on Building Insurance Through Rate Comparison

A systematic rate comparison significantly reduces your insurance costs without giving up important coverage. Many consumers save substantially on building insurance through rate comparisons — often several hundred euros per year. The process is simpler than most people think.

Determine the exact value of your building based on living space and construction type.

Decide which risks you want to insure, especially whether natural hazard coverage is necessary.

Use a comparison portal and enter all relevant building data.

Compare at least five to seven offers in terms of price and coverage.

Check the contract terms carefully, especially exclusions and deductibles.

Watch out for hidden costs such as processing fees or payment surcharges.

Comparison portals offer the advantage of reviewing dozens of rates in just minutes. The input forms guide you through all important questions. You receive a clear list with premiums and coverage features. This saves time and ensures you don't overlook important providers.

Special building features affect the price. Energy-efficient houses with modern insulation receive discounts from some insurers. Solar panels on the roof, however, often increase the premium as they represent additional damage risk during storms or hail. Older buildings with outdated electrics or heating are considered high-risk and cost more.

Pro Tip

Pay special attention to the underinsurance waiver clause. It should apply unconditionally, not only when the insured sum is adjusted annually. Some insurers tie the waiver to specific calculation methods like the 1914 value index. Read the fine print carefully.

“A thorough rate comparison always pays off. Even with identical coverage, premiums from different providers differ by 30 to 40 percent. Anyone who compares and switches every three years saves thousands of euros in the long run.”

When comparing building insurance rates, also consider customer reviews and claims handling. A cheap rate is of little use if the insurer pays slowly or refuses benefits in the event of a claim. Check experience reports and complaint statistics from the insurance supervisory authority (BaFin).

Remember that insurance companies regularly adjust their premiums. What's cheap today may be expensive in two years. Review your contract at least every three years and use your special cancellation right (Sonderkündigungsrecht) when premiums increase. This keeps you flexible and ensures you benefit from favorable conditions long-term.

Common Claims and How Building Insurance Helps

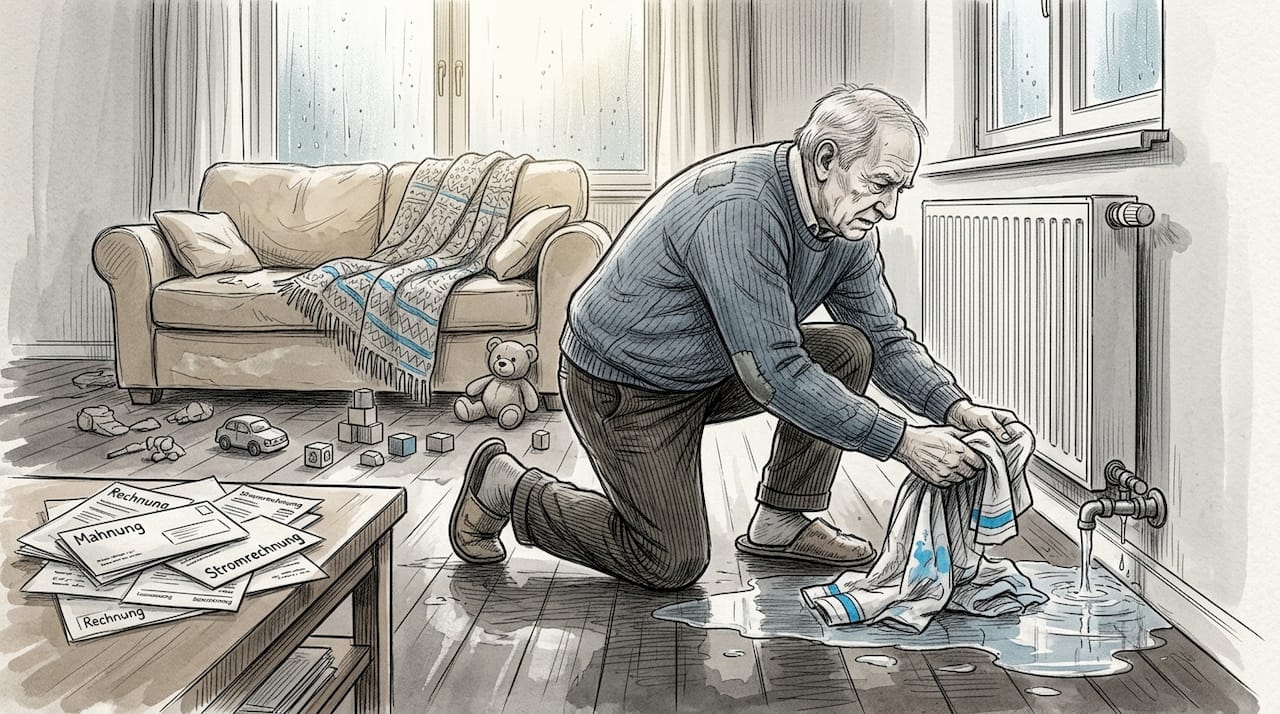

Building insurance proves its value when a claim occurs. Damage from pipe bursts, fire, or storms are the most common causes of claims in residential buildings, and the financial consequences can be devastating.

A pipe burst in winter is one of the most typical claims. Frozen pipes burst and water runs unnoticed into walls and floors for hours. The result: soaked walls, destroyed floors, and mold formation. Repair costs quickly reach €20,000 to €50,000. Building insurance covers drying costs, renovation, and restoration.

Fire damage from lightning strikes or technical defects often destroys entire building sections. An attic fire can spread within minutes. Even if the fire department extinguishes quickly, massive damage from soot, heat, and extinguishing water remains. The insurance pays for reconstruction, disposal, and temporary accommodation for residents.

Storm damage occurs especially in autumn and winter. Hurricanes tear off roof tiles, damage facades, or throw trees onto buildings. It's important to note that insurance only covers from wind force 8. Document damage immediately with photos and report it without delay.

| Claim Type | Common Cause | Avg. Cost | Insurance Benefit |

|---|---|---|---|

| Pipe Burst | Frost damage, material fatigue | €15,000 to €40,000 | Repair, drying, renovation |

| Fire | Lightning, electrical defect | €80,000 to €200,000 | Rebuild, cleanup, hotel costs |

| Storm Damage | Gales from wind force 8 | €8,000 to €25,000 | Roof repair, facade renovation |

| Hail Damage | Severe weather with large hailstones | €5,000 to €15,000 | Roof tiles, windows, shutters |

When reporting a claim, you must act quickly. Inform your insurance within 48 hours. Document everything with photos and videos. Don't remove any evidence before the assessor has visited. You have a duty to mitigate damage — meaning you must prevent further damage, for example by covering damaged roofs.

Building insurance for pipe bursts also covers hidden damage. If a pipe in the wall is leaking and isn't discovered for months, the insurance still pays. The prerequisite is that you have properly maintained the building.

Natural hazard damage such as flooding or heavy rain is only covered with additional coverage. After the devastating floods of recent years, many homeowners have booked this option retroactively. In some regions, natural hazard coverage is difficult or impossible to obtain. Find out early about availability in your area.

It's also important to distinguish between pipe water and rainwater. If rain enters through a leaky roof, only storm coverage applies — and only if the storm damaged the roof. If a heating pipe leaks, however, the water pipe insurance pays. This distinction often leads to misunderstandings.

Find the Best Building Insurance and Save

You now have the knowledge to make an informed decision. The next step is a practical comparison of current rates. On meinetarife24.de you'll find a clear platform that helps you quickly and transparently find the best offers for your building insurance.

Our comparison calculator considers all important factors such as building value, construction type, and desired additional options. You'll receive a list of matching rates with detailed coverage overviews within minutes.

Frequently Asked Questions About Building Insurance

What is the difference between building insurance and contents insurance?

Building insurance protects the structure of your house — walls, roof, and permanently installed elements. Contents insurance covers movable items like furniture, electronics, and clothing. Both complement each other but cover entirely different areas.

What damage is covered by building insurance?

Basic coverage includes damage from fire, water pipes, storms from wind force 8, and hail. With natural hazard coverage (Elementarschutz), you extend protection to flooding, heavy rain, landslides, and snow pressure. Vandalism and gross negligence can be optionally insured.

Can I take out building insurance as a tenant?

No, building insurance can only be taken out by the property owner. As a tenant, you need contents insurance for your belongings and possibly private liability insurance. The landlord is obligated to insure the building itself.

How important is the underinsurance waiver?

The underinsurance waiver (Unterversicherungsverzicht) is extremely important. It guarantees that the insurance covers the full costs in the event of a claim, even if the insured sum was set too low. Without this clause, you risk significant out-of-pocket costs with every claim.

Is it worth switching building insurance?

Switching is almost always worthwhile if you find a cheaper rate with equal or better coverage. Insurance companies regularly adjust their premiums, so you should compare every three years. Use your special cancellation right (Sonderkündigungsrecht) when premiums increase to stay flexible.