Key Takeaways at a Glance

| Key Point | Details |

|---|---|

| Follow a structured approach | A step-by-step guide simplifies the selection process and saves time |

| Know the insurance types | Haftpflicht, Teilkasko, and Vollkasko offer different levels of protection for different needs |

| Use comparison tools | Online calculators provide quick access to affordable rates and transparent price comparisons |

| Avoid common mistakes | A checklist helps you avoid typical pitfalls when signing up for insurance |

| Review regularly | Annual insurance reviews ensure lasting savings and optimal coverage |

Understanding Car Insurance Basics

Before you start comparing, it helps to know the three coverage levels and a few key terms. German car insurance (German: Kfz-Versicherung) comes in three tiers, each covering a different range of risks.

Haftpflichtversicherung (Third-Party Liability)

Mandatory by law. This is the minimum cover required to drive in Germany. It pays for damage you cause to other vehicles, people, or property. Without it you cannot register your car or drive on public roads. The legal minimum limits are set by federal regulation (German: Pflichtversicherungsgesetz).

Teilkasko (Partial Coverage)

Adds protection for your own vehicle against specific events: theft, fire, glass damage, hail, storm, flooding, and collisions with game (German: Haarwild, e.g. deer or wild boar). Note that collisions with other animals are only covered if your policy explicitly includes Tiere aller Art. Useful for cars that still hold meaningful value but are past their first few years.

Vollkasko (Comprehensive Coverage)

The broadest cover available. On top of everything Teilkasko includes, it also pays for damage caused by your own driving mistake and for vandalism. Recommended for new or high-value cars. As a car ages and loses value, the benefit of Vollkasko decreases, so it makes sense to revisit this each year.

Key German Terms You Should Know

Selbstbeteiligung

Deductible

The amount you pay out of pocket before insurance kicks in

Schadenfreiheitsrabatt

No-Claims Discount

Discount for accident-free years that significantly lowers your premium

Regionalklasse

Regional Class

Classification based on accident frequency in your area of residence

Typklasse

Vehicle Type Class

Rating of your vehicle model based on claim frequency and repair costs

Pro Tip

Write down any terms you do not immediately understand when reading through for the first time, and clarify them before comparing. A solid basic understanding prevents you from overlooking or misinterpreting important contract details later on.

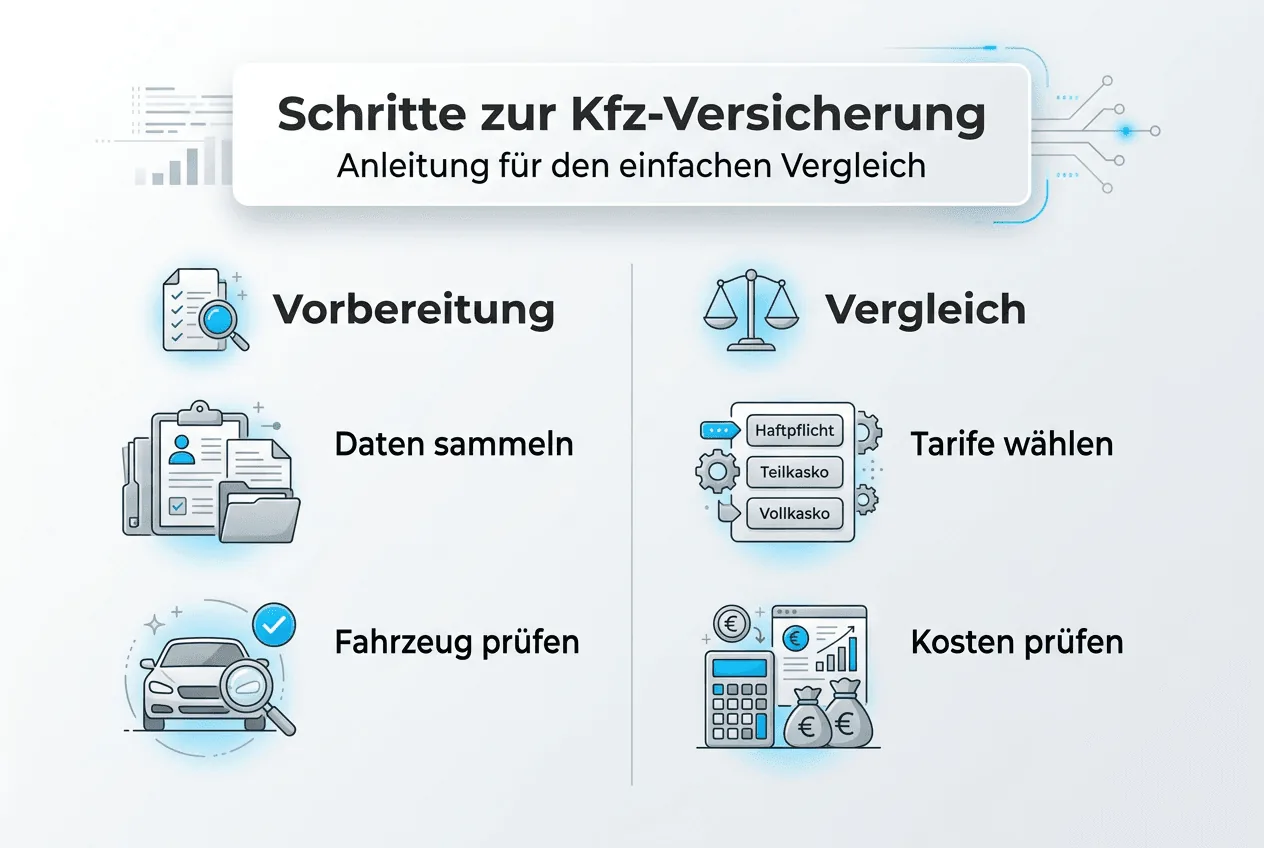

Preparation: Setting Your Personal Requirements

Before comparing rates, gather your vehicle information and personal data. Things like your age, where you live, and your claims history all affect the premium. The more complete your details, the more accurate the comparison results.

Vehicle Data You Will Need

- Make, model, and exact type designation of your car

- First registration date and current mileage

- HSN and TSN from your vehicle registration document (Fahrzeugschein)

- Information about special equipment like navigation systems or parking assistants

Your personal details matter just as much. Insurers consider your date of birth, as younger drivers statistically cause more accidents. Your place of residence determines the regional class (German: Regionalklasse), which varies by accident frequency in each area. Annual mileage also plays a role: more kilometres driven means a higher statistical risk.

Special circumstances can lower your premium. Do you have a garage or a fixed parking spot? Is this a second vehicle? Does your car have modern safety systems like automatic emergency braking or lane departure warning? Each of these factors can have a positive impact on your annual premium.

Deductible Tip

Think ahead about what deductible you could cover in a claim situation. A higher deductible noticeably lowers your annual premium, but it means higher out-of-pocket costs when something happens. Finanztip suggests around EUR 150 for Teilkasko and EUR 300 for Vollkasko as a reasonable starting point for most drivers.

If you are new to Germany and drove abroad before, your existing no-claims history may count toward your German Schadenfreiheitsklasse. See the FAQ section below for the rules on recognition.

Selection and Comparison: Comparing Step by Step

Now the actual comparison begins. Online comparison tools help you quickly find tariffs that fit your situation. Approach this step by step so you do not miss anything important.

Enter Your Rate Criteria

Open a comparison tool and enter all your prepared data completely. Pay special attention to your no-claims class (German: Schadenfreiheitsklasse), as this has the biggest single impact on your premium. Then select your desired coverage level.

Review the Offers

Do not sort results only by the lowest price. Look at the scope of coverage too. A low premium is not helpful if key benefits are missing or if claims processing is slow.

Compare Coverage Features

Check which extras are included. Some tariffs offer no-claims protection (German: Rabattschutz), marten-bite follow-up damage coverage, or a gross-negligence waiver. These can be valuable in an emergency and are worth checking even in budget tariffs.

Identify Discounts

Many insurers offer special rates for certain professions, garage users, or when you bundle multiple contracts. Check which discounts apply to your situation.

Make Your Final Decision

Pick the policy with the best overall value for your situation. The cheapest option is rarely the best if it leaves out coverage you actually need.

Pro Tip

Note down the three to five most interesting offers with their specific coverage features alongside the price. This helps you keep track and make a well-informed decision rather than just going by the headline number.

| What to compare | What matters |

|---|---|

| Annual premium | Compare the yearly total, not the monthly instalment — annual payment is usually cheaper |

| Deductible (Selbstbeteiligung) | Finanztip suggests around EUR 150 for Teilkasko and EUR 300 for Vollkasko as a useful orientation |

| No-claims protection (Rabattschutz) | Keeps your discount class after a claim — worth it if you have a high no-claims level |

| Workshop restriction (Werkstattbindung) | Some cheaper tariffs require you to use a partner garage; check whether that suits you |

| Claims benefits | Look for marten-bite follow-up damage coverage, gross-negligence waiver, and new-for-old replacement |

Compare Car Insurance Now

The comparison is free and your data is processed in line with the GDPR. Enter your details and see results from our partner Tarifcheck, which covers 300+ car insurance tariffs from 40+ insurers.

Disclosure: This comparison is free for you. If you sign up through our comparison partner, we earn a commission. This does not change the results shown.

Data Source & Transparency

The tariff data on this page is provided in real-time by Tarifcheck. We do not alter prices, rankings, or how results are displayed.

Our role:

We provide editorial explanations and decision-making guidance. The actual tariff calculation and mediation is done by our partners.

What we do not cover:

Not all providers in the market are included in this comparison. Regional providers or specialized tariffs may be missing.

Online Application and Contract Review

After choosing a policy, the sign-up process follows. Many people make avoidable mistakes at this stage. Read the contract terms carefully before confirming anything.

Pay Attention to These Contract Details

Exclusions (Ausschlüsse)

Which damages are explicitly not covered? Some policies exclude marten bite follow-up damage or certain weather events.

Contract Duration (Vertragslaufzeit)

Most policies run for one year with automatic renewal. Check the cancellation deadline, usually one month before contract end.

Payment Method (Zahlungsweise)

Annual payment is usually cheaper than monthly installments. Some insurers add surcharges for installment payment.

Workshop Restriction (Werkstattbindung)

Some cheaper tariffs require you to use a partner workshop for repairs. That limits your choice of garage, so decide whether the savings are worth it.

Enter all personal data correctly and completely. Incorrect information can lead to loss of coverage when you make a claim. Particularly sensitive are your no-claims class, driver circle details, and annual mileage. If you are unsure, choose a slightly higher mileage rather than one that is too low.

eVB Number (elektronische Versicherungsbestätigung)

After signing up, you receive the electronic insurance confirmation. This 7-character code is required to register your vehicle at the registration office (German: Zulassungsstelle). Keep all documents safe.

"A thorough review of contract terms before signing prevents unpleasant surprises in case of a claim and secures the agreed protection."

Check the confirmation email and insurance policy carefully for accuracy. Do all details match your information? Does the premium match the displayed offer? If there are discrepancies, contact the insurer immediately.

Common Mistakes and Optimization

Signing up is not the end of the process. A regular insurance check can save money and prevents you from being over-insured. Review your contract at least once a year, ideally before November 30, the last day for regular cancellations that take effect at year-end.

Typical Mistakes to Avoid

Incorrect Mileage (Kilometerangaben)

Stating too low a mileage can cause problems in case of a claim.

Concealed Prior Damage (Vorschaeden)

Unreported prior accidents can jeopardize your insurance coverage.

Missed Cancellation Deadlines (Kündigungsfristen)

The one-month deadline before contract end must be observed strictly. Miss it and you are locked in for another year.

Ignoring Automatic Renewal

Without cancellation, the contract automatically continues for another year.

How to Switch to a Cheaper Provider

- 1Compare current rates no later than October or November

- 2Cancel your old contract in writing, ideally by registered mail (Einschreiben)

- 3Only sign the new contract after receiving cancellation confirmation

- 4Ensure seamless insurance coverage during the switch

- 5Inform the registration office (Zulassungsstelle) about the insurance change

Optimize your insurance to match your current situation. Is your car driving fewer kilometres than originally stated? Have you moved? Do you now park in a garage? All these changes can lower your premium. Report them to your insurer promptly.

When to Downgrade Coverage

For older cars, check whether Vollkasko is still worthwhile. According to Finanztip, if your car is older than about five years and its residual value is low, Teilkasko is usually sufficient. For very old cars with minimal remaining value, even just third-party liability may be enough. Reviewing this annually helps you avoid paying for cover that no longer makes financial sense.

Save with meinetarife24

You now know how to find the right car insurance in Germany step by step. meinetarife24 gives you the tools to put that into practice. As a newcomer or expat, you get the same comparison options as any German resident, explained in plain language.

Use our car insurance comparison to find tariffs from our partner Tarifcheck, which covers 300+ car insurance tariffs from 40+ insurers. The online process is straightforward: enter your details, compare offers, and sign up directly. According to Finanztip and Stiftung Warentest, switching providers can mean savings of several hundred euros per year, depending on your vehicle and situation.

Already covered but wondering if you pay too much? Check our car insurance cost guide and the car insurance checklist to prepare properly. If you came from abroad and want to know how your existing no-claims history transfers, the SF class guide explains the rules in detail.

Prefer a budget tariff? The cheap car insurance guide covers what to watch out for when picking a low-cost option. The comparison is free and your data is processed in line with the GDPR.

Frequently Asked Questions

What car insurance do I need at minimum in Germany?

At minimum, third-party liability insurance (Haftpflichtversicherung) is legally required, and without it you may not operate your vehicle on public roads. It covers damage you cause to other vehicles, people, or property. The legal minimum coverage limits are set by federal regulation. For extra protection you can add Teilkasko (partial) or Vollkasko (comprehensive) cover.

How can I save money on car insurance?

Compare multiple providers before signing to find the best value. Use the no-claims discount (Schadenfreiheitsrabatt) by driving accident-free. Adjust your deductible to your financial situation; a higher deductible lowers your annual premium. Report changes like garage use or lower mileage promptly, as these reduce costs. Paying annually rather than monthly also avoids instalment surcharges.

When should I switch my car insurance?

Review your contract each year and consider switching when you find significantly better offers with comparable or improved coverage. After major life changes (new address, new car, changed mileage), a different policy may suit you better. Always observe the cancellation deadline of one month before contract end; for policies ending December 31, this means cancelling by November 30.

What data do I need for the online application?

You need complete vehicle details: make, model, year, HSN (manufacturer code), TSN (type code), and annual mileage. Personal information includes your name, address, date of birth, and details about the driver circle (Fahrerkreis). You also need your current no-claims class and your desired coverage level with deductible amount. Have your payment information ready to complete the process.

Will my no-claims discount from abroad be recognised?

It depends on where you drove before. For EU and EEA countries, German insurers are required by law to recognise your foreign no-claims history. This obligation applies since 17 April 2024 under EU regulation 2021/2118. For non-EEA countries such as Turkey, the USA, or Switzerland, recognition is at the discretion of the individual insurer. Ask your previous insurer for a confirmation letter (Schadensfreiheitsbescheinigung) in any case, as some German insurers will consider it even when not legally required.